Matt Breese

Matt Breese

The Category Making News Is Not the Category You're Building In

The bourbon glut story has gone fully mainstream. It is in the Wall Street Journal. It is in hospitality industry newsletters. It is moving through...

The bourbon glut story has gone fully mainstream. It is in the Wall Street Journal. It is in hospitality industry newsletters. It is moving through...

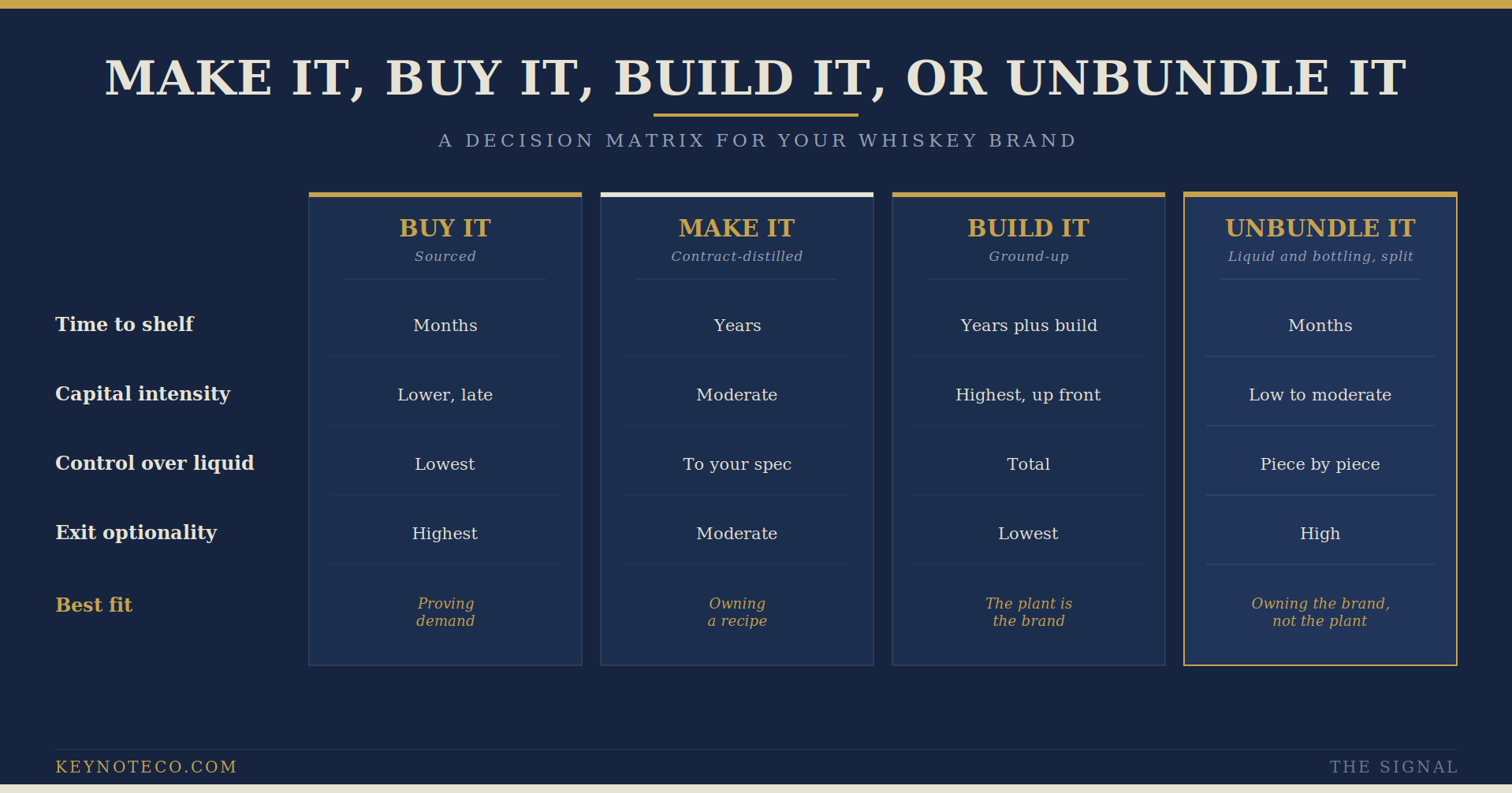

Most people choosing how to make their whiskey are answering the wrong question. They ask which path is most legitimate, or which one a serious brand...

Launching a whiskey brand is an exciting endeavor, but it comes with structural realities that many first-time founders underestimate. Chief among...