Matt Breese

Matt Breese

The Label Knows First: What TTB Approvals Reveal About Where Whiskey Brands Are Heading

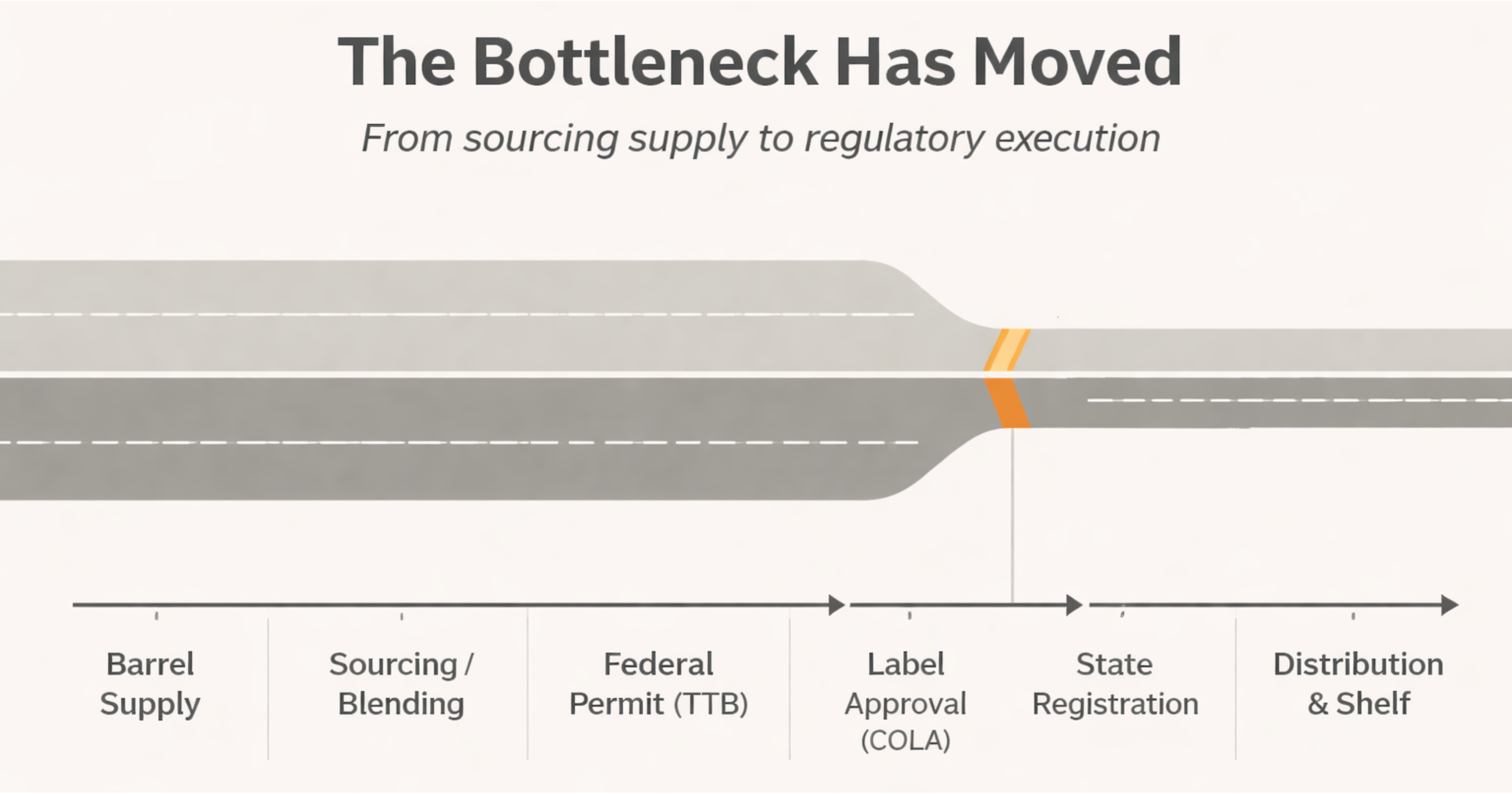

There is a number that does not get talked about enough in whiskey circles: the monthly count of new label approvals coming out of the Alcohol and...

There is a number that does not get talked about enough in whiskey circles: the monthly count of new label approvals coming out of the Alcohol and...

How a finishing-obsessed “mad scientist” ethos, a musician’s eye for album art, and a flavor-first stance are reshaping what 95/5 rye can be.

The whiskey industry is entering a new phase—one defined not by expansion at all costs, but by balance. After years of aggressive production, rising...