Matt Breese

Matt Breese

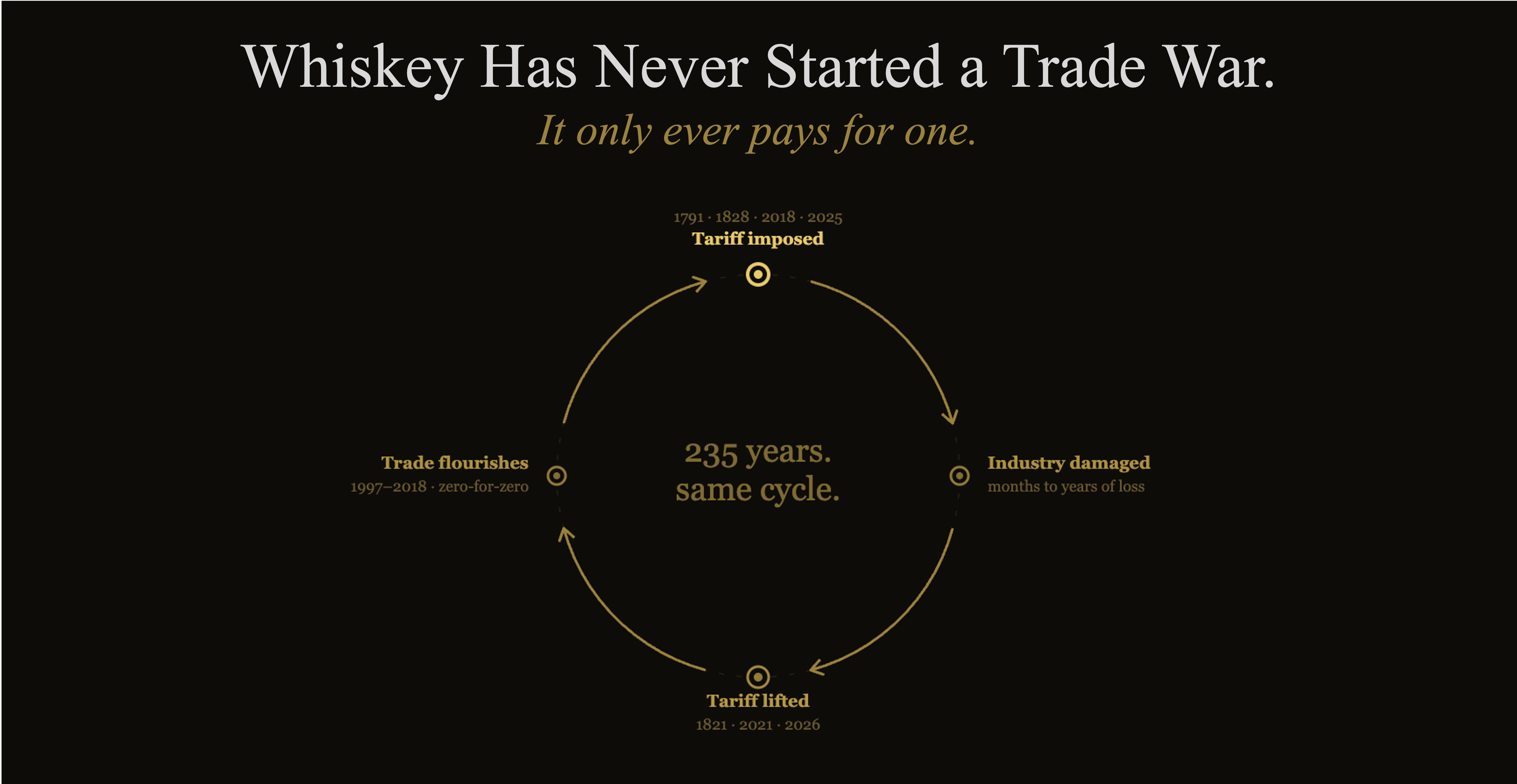

Whiskey Has Never Started a Trade War. It Only Ever Pays for One.

On April 30, 2026, President Trump announced the removal of the 10% tariff on Scotch whisky imports to the United States. He posted it on Truth...

On April 30, 2026, President Trump announced the removal of the 10% tariff on Scotch whisky imports to the United States. He posted it on Truth...

The bourbon glut story has gone fully mainstream. It is in the Wall Street Journal. It is in hospitality industry newsletters. It is moving through...

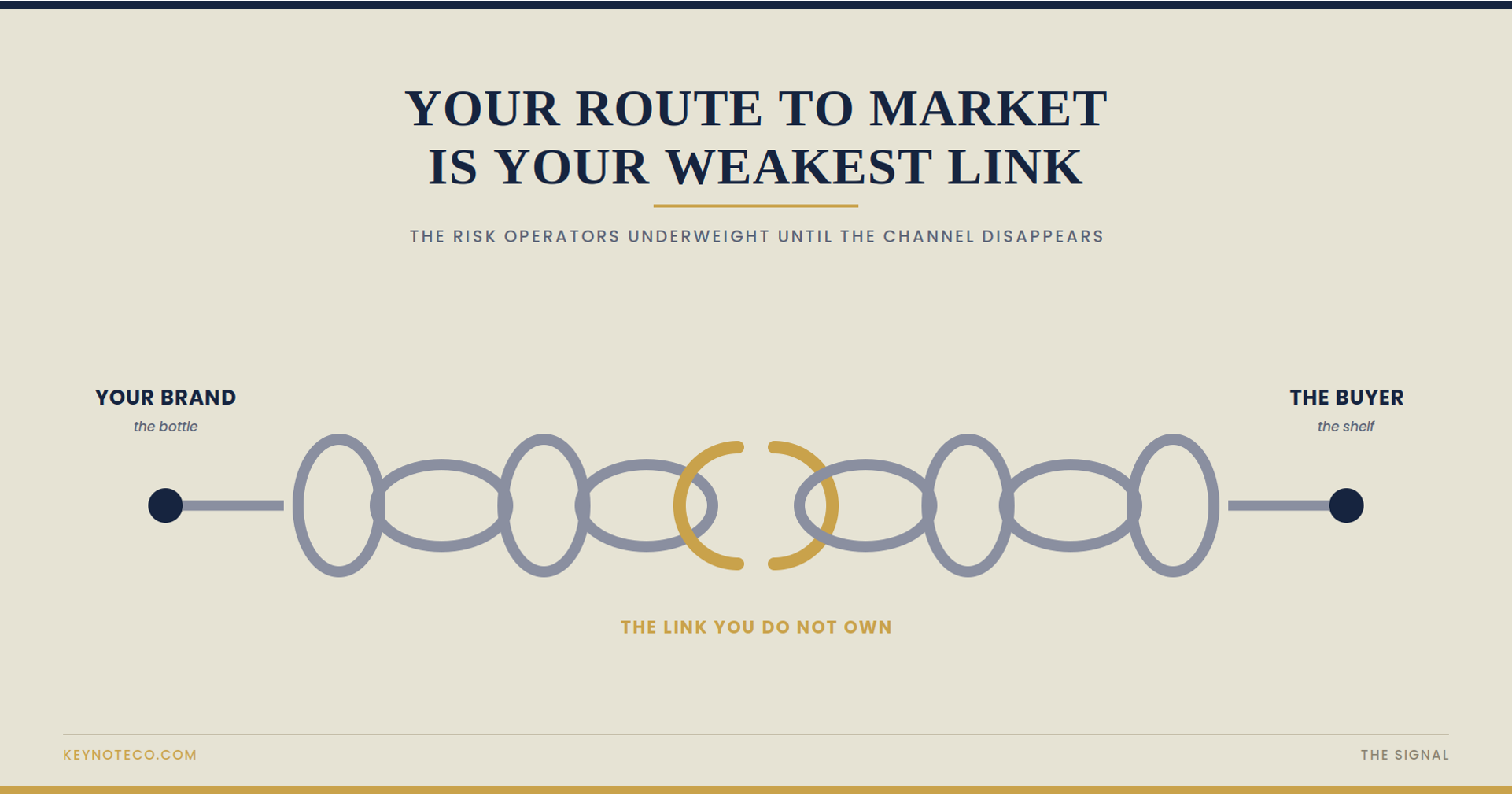

Ask a whiskey operator to name the risks to their brand and you will get a predictable list. The liquid might not be good enough. The price might be...